Related Distributions

- If is a normal distribution, then

- If is distributed log-normally, then is a normal random variable.

- If are n independent log-normally distributed variables, and, then Y is also distributed log-normally:

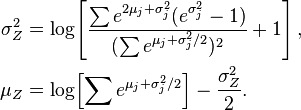

- Let be independent log-normally distributed variables with possibly varying σ and μ parameters, and . The distribution of Y has no closed-form expression, but can be reasonably approximated by another log-normal distribution Z at the right tail. Its probability density function at the neighborhood of 0 has been characterized and it does not resemble any log-normal distribution. A commonly used approximation (due to Fenton and Wilkinson) is obtained by matching the mean and variance:

In the case that all have the same variance parameter, these formulas simplify to

- If, then X + c is said to have a shifted log-normal distribution with support x ∈ (c, +∞). E = E + c, Var = Var.

- If, then

- If, then

- If then for

- Lognormal distribution is a special case of semi-bounded Johnson distribution

- If with, then (Suzuki distribution)

Read more about this topic: Log-normal Distribution

Famous quotes containing the word related:

“In the middle years of childhood, it is more important to keep alive and glowing the interest in finding out and to support this interest with skills and techniques related to the process of finding out than to specify any particular piece of subject matter as inviolate.”

—Dorothy H. Cohen (20th century)

Related Phrases

Related Words