General Multidimensional Distributions

Remember that the cumulative distribution function for a vector of random variables is defined in terms of their joint probability distribution;

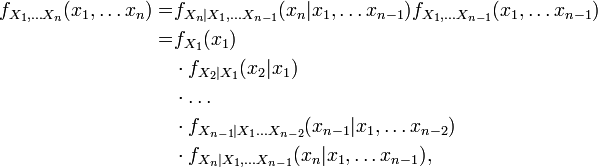

The joint distribution for two random variables can be extended to many random variables X1, ... Xn by adding them sequentially with the identity

where

and

(notice, that these latter identities can be useful to generate a random variable with given distribution function ); the density of the marginal distribution is

The joint cumulative distribution function is

and the conditional distribution function is accordingly

Expectation reads

suppose that h is smooth enough and for, then, by iterated integration by parts,

Read more about this topic: Joint Probability Distribution

Famous quotes containing the word general:

“I suggested to them also the great desirability of a general knowledge on the Island of the English language. They are under an English speaking government and are a part of the territory of an English speaking nation.... While I appreciated the desirability of maintaining their grasp on the Spanish language, the beauty of that language and the richness of its literature, that as a practical matter for them it was quite necessary to have a good comprehension of English.”

—Calvin Coolidge (1872–1933)