Explanation

Contribution margin can be thought of as the fraction of sales that contributes to the offset of fixed costs. Alternatively, unit contribution margin is the amount each unit sale adds to profit: it's the slope of the Profit line.

Cost-Volume-Profit Analysis (CVP): assuming the linear CVP model, the computation of Profit and Loss (Net Income) reduces as follows:

where TC = TFC + TVC is Total Cost = Total Fixed Cost + Total Variable Cost and X is Number of Units. Thus Profit is Unit Contribution times Number of Units, minus the Total Fixed Costs.

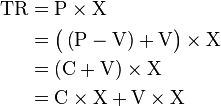

The above formula is derived as follows:

From the perspective of the matching principle, one breaks down the revenue from a given sale into a part to cover the Unit Variable Cost, and a part to offset against the Total Fixed Costs. Breaking down Total Costs as:

one breaks down Total Revenue as:

Thus the Total Variable Costs offset, and the Net Income (Profit and Loss) is Total Contribution Margin minus Total Fixed Costs:

Read more about this topic: Contribution Margin

Famous quotes containing the word explanation:

“To develop an empiricist account of science is to depict it as involving a search for truth only about the empirical world, about what is actual and observable.... It must involve throughout a resolute rejection of the demand for an explanation of the regularities in the observable course of nature, by means of truths concerning a reality beyond what is actual and observable, as a demand which plays no role in the scientific enterprise.”

—Bas Van Fraassen (b. 1941)

“There is no explanation for evil. It must be looked upon as a necessary part of the order of the universe. To ignore it is childish, to bewail it senseless.”

—W. Somerset Maugham (1874–1965)

“How strange a scene is this in which we are such shifting figures, pictures, shadows. The mystery of our existence—I have no faith in any attempted explanation of it. It is all a dark, unfathomed profound.”

—Rutherford Birchard Hayes (1822–1893)