Life Insurance

Whole life insurance pays a pre-determined benefit either at or soon after the insured's death. The symbol (x) is used to denote "a life aged x" where x is a non-random parameter that is assumed to be greater than zero. The actuarial present value of one unit of whole life insurance issued to (x) is denoted by the symbol or in actuarial notation. Let G>0 (the "age at death") be the random variable that models the age at which an individual, such as (x), will die. And let T (the future lifetime random variable) be the time elapsed between age-x and whatever age (x) is at the time the benefit is paid (even though (x) is most likely dead at that time). Since T is a function of G and x we will write T=T(G,x). Finally, let Z be the present value random variable of a whole life insurance benefit of 1 payable at time T. Then:

where i is the effective annual interest rate and δ is the equivalent force of interest.

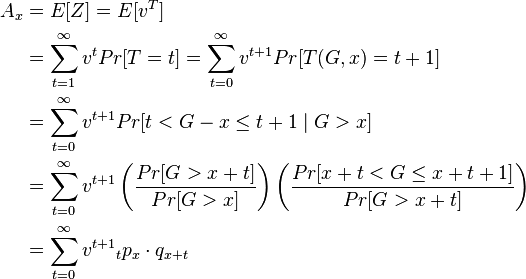

To determine the actuarial present value of the benefit we need to calculate the expected value of this random variable Z. Suppose the death benefit is payable at the end of year of death. Then T(G, x) := ceiling(G - x) is the number of "whole years" (rounded upwards) lived by (x) beyond age x, so that the actuarial present value of one unit of insurance is given by:

where is the probability that (x) survives to age x+t, and is the probability that (x+t) dies within one year.

If the benefit is payable at the moment of death, then T(G,x): = G - x and the actuarial present value of one unit of whole life insurance is calculated as

where is the probability density function of T, is the probability of a life age surviving to age and denotes force of mortality at time for a life aged .

The actuarial present value of one unit of an n-year term insurance policy payable at the moment of death can be found similarly by integrating from 0 to n.

The actuarial present value of an n year pure endowment insurance benefit of 1 payable after n years if alive, can be found as

In practice the information available about the random variable G (and in turn T) may be drawn from life tables, which give figures by year. For example, a three year term life insurance of $100,000 payable at the end of year of death has actuarial present value

For example, suppose that there is a 90% chance of an individual surviving any given year (i.e. T has a geometric distribution with parameter p = 0.9 and the set {1, 2, 3, ...} for it's support). Then

and at interest rate 6% the actuarial present value of one unit of the three year term insurance is

so the actuarial present value of the $100,000 insurance is $24,244.85.

In practice the benefit may be payable at the end of a shorter period than a year, which requires an adjustment of the formula.

Read more about this topic: Actuarial Present Value

Famous quotes containing the words life and/or insurance:

“That which resembles most living one’s life over again, seems to be to recall all the circumstances of it; and, to render this remembrance more durable, to record them in writing.”

—Benjamin Franklin (1706–1790)

“For there can be no whiter whiteness than this one:

An insurance man’s shirt on its morning run.”

—Gwendolyn Brooks (b. 1917)