Related Distributions

- If is a normal distribution, then

- If is distributed log-normally, then is a normal random variable.

- If are n independent log-normally distributed variables, and, then Y is also distributed log-normally:

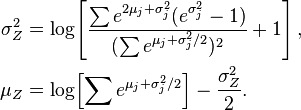

- Let be independent log-normally distributed variables with possibly varying σ and μ parameters, and . The distribution of Y has no closed-form expression, but can be reasonably approximated by another log-normal distribution Z at the right tail. Its probability density function at the neighborhood of 0 has been characterized and it does not resemble any log-normal distribution. A commonly used approximation (due to Fenton and Wilkinson) is obtained by matching the mean and variance:

In the case that all have the same variance parameter, these formulas simplify to

- If, then X + c is said to have a shifted log-normal distribution with support x ∈ (c, +∞). E = E + c, Var = Var.

- If, then

- If, then

- If then for

- Lognormal distribution is a special case of semi-bounded Johnson distribution

- If with, then (Suzuki distribution)

Read more about this topic: Log-normal Distribution

Famous quotes containing the word related:

“Perhaps it is nothingness which is real and our dream which is non-existent, but then we feel think that these musical phrases, and the notions related to the dream, are nothing too. We will die, but our hostages are the divine captives who will follow our chance. And death with them is somewhat less bitter, less inglorious, perhaps less probable.”

—Marcel Proust (1871–1922)

Related Phrases

Related Words